What's the Difference Between FHA and Conventional Mortgage Loans?

Federal Housing Administration (FHA) loans are in a category of mortgages called government-insured mortgage loans. Examples of government-insured (also known as government-backed) mortgage loans are Veterans Administration (VA) and United States Department of Agriculture (USDA) mortgage loans.

Conventional loans are backed by or insured by private lenders and are not government-backed or government-insured.

The FHA loan was created to help a wide range of homebuyers (such as first-time buyers and seniors) become homeowners. Homeownership is more accessible with an FHA loan because government-backed mortgage loans have more relaxed qualifying requirements than conventional mortgage loans that are provided by private lenders.

FHA-approved lenders include credit unions, banks, and online lenders, which also offer conventional and government-backed loans.

At Credit Union of Southern California (CU SoCal), we make getting FHA and conventional mortgage loans easy!

Call 866.287.6225 today to schedule a no-obligation consultation and learn about our

mortgages,

home equity lines of credit,

auto loans,

personal loans,

checking and

savings accounts, and other banking products. As a full-service financial institution, we look forward to helping you with all of your banking needs.

What are the differences between FHA vs. conventional loans? Read on to learn more!

Get Started on Your Mortgage Today!

What are FHA Loans?

FHA loans have been helping people become homeowners since 1934. The Federal Housing Administration (FHA) is part of the

U.S. Department of Housing and Urban Development, and provides mortgage insurance on loans made by FHA-approved lenders. If a property owner defaults on their mortgage, the FHA will pay a claim to the lender for the unpaid principal balance. Because lenders take on less risk, they are able to offer more mortgage options to homebuyers with lower credit scores and even lower income.

The FHA insures mortgages on single-family homes, and multifamily properties, throughout the United States and its territories.

Homebuyers benefit from FHA loans because FHA-approved lenders can offer homebuyers better loan terms, including:

- Down payments as low as 3.5%.

- Lower closing costs.

- Lower qualifying credit scores:

- Borrowers with a credit score at or above 580 to be eligible for maximum financing.

- Borrowers with a minimum credit score between 500 and 579 are limited to 90 percent LTV financing.

- Borrowers with credit score of less than 500 are not eligible for FHA-insured mortgage financing. Have bad credit? There are ways to build your credit score.

What are Conventional Loans?

As we mentioned earlier, conventional mortgage loans are offered and insured by private lenders that may include credit unions, banks, and online lenders.

Conventional loans tend to be better for homebuyers with excellent credit, steady income, and lower debt.

There are two categories of conventional loans: "conforming" and "non-conforming."

Conforming Conventional mortgage loans conform to guidelines set by Freddie Mac (Federal Home Loan Mortgage Corporation) and Fannie Mae (Federal National Mortgage Association), agencies that were created by Congress to provide liquidity, stability, and affordability to the mortgage market.

These agencies provide thousands of banks, savings and loans, and mortgage companies with ready access to funds on reasonable terms, which are then used to make mortgage loans for consumers.

Non-Conforming Conventional Loans. These are loans that do not conform to Freddie Mac and Fannie Mae guidelines. One example of non-conforming loans is a Jumbo loan, used for large mortgage amounts.

While FHA loans are not conventional, they are also considered non-conforming because they don’t conform to the Freddie Mac and Fannie Mae guidelines.

To be approved for a conventional mortgage loan, a borrower typically needs to satisfy the following requirements (which may vary slightly by lender):

- A credit score of 620 or higher.

- Debt-to-Income (DTI) ratio up of 50%. The required ratio may depend on the lender’s requirements, the borrower’s credit score, and other factors.

- Conforming Loan Limit. According to the Federal Housing Finance Agency (FHFA), the conforming loan limits (CLLs) for mortgages to be acquired by Fannie Mae and Freddie Mac (the Enterprises) in most of the U.S. for one-unit properties is $647,200. A homebuyer needed a larger loan amount would apply for a jumbo loan.

Borrowers who make a down payment of less than 20 percent will typically be required by a lender to pay Private Mortgage Insurance (PMI). PMI is added to the borrower’s monthly mortgage payment to protect the lender financially if the borrower defaults. Once 20 percent equity in the home is reached, PMI can be waived.

In an FHA loan scenario HUD collects mortgage insurance premiums from borrowers via lenders. HUD uses this income to operate its mortgage insurance programs for the benefit of homebuyers, renters, and communities.

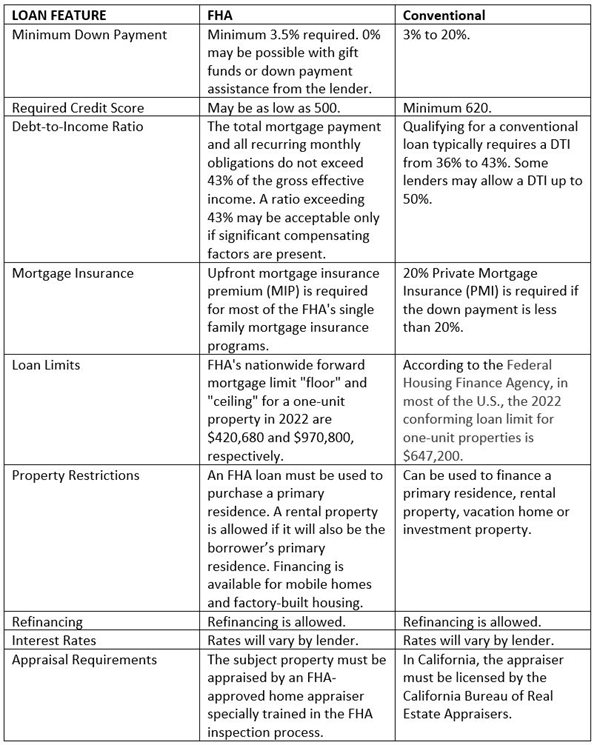

Comparing FHA vs. Conventional Loans

Which Loan Is Right For Me?

Many homebuyers ask, which is better an FHA or conventional loan? Deciding between a conventional mortgage vs. FHA loan should be based on several factors including your income stream and job stability, how long you plan to stay in the home, how much you can afford in monthly mortgage payments, etc.

At Credit Union of Southern California we’ll help you evaluate the options so you choose the loan that works best for your unique situation.

Here are some tips for deciding

how much house you can afford.

When You Should Consider a Conventional Loan:

If you have:

- A credit score greater than 620.

- Steady income

- Long work history

- Money for a down payment of more than 3.5% of the property purchase price.

When You Should Consider an FHA Loan:

If you:

- Are a first-time homebuyer or senior.

- Have limited savings for a down payment.

- Have a low credit score.

- Are purchasing a manufactured home.

Use this

mortgage payment calculator to see what size mortgage you can afford.

How to Apply for an FHA or Conventional Loan

The loan application process is basically the same no matter which type of loan you choose. The lender you choose will ask permission to view your credit score, and ask you supply proof of income and debt, tax returns, and bank statements

- First, determine how much home you can afford.

- Shop for a loan by speaking to different lenders. (CU SoCal has FHA loans!)

- Learn about FHA loans. Your lender can provide you with details on the types of FHA loan programs they offer.

- Get pre-approved by the lender.

- Shop for a home

- Make an offer.

- Complete the mortgage application process.

- Get a home inspection

- For an FHA loan, the home will need to be evaluated by an FHA-approved property appraiser.

- Shop for homeowners insurance.

- Sign the closing document.

Learn

how to save money for a house.

Why Consumers Choose CU SoCal

For over 60 years CU SoCal has been providing financial services, including mortgages, Home Equity Loans, HELOCs, car loans, personal loans, credit cards, and other banking products, to those who live, work, worship, or attend school in Orange County, Los Angeles County, Riverside County, and San Bernardino County.

Please give us a call today at 866.287.6225 today to schedule a no-obligation loan consultation with a CU SoCal Member Services specialist.

Get Started on Your Mortgage Today!